Money Matters & 9/11: Delving into Darker Truths

Sunday, 11. September 2011

Money matters provide some of most compelling unanswered questions regarding the events of September 11, 2001. These questions point to possible darker truths, in part because of the incomplete and/or misleading treatments in official investigations to date. Pressing questions remain in at least three issue areas, including money transfers, suspicious activity reporting, and informed securities trading. In turn, cursory and misleading conclusions among relevant investigatory parties suggest a cover-up consistent with the possibility that the crimes of 9/11 were allowed to happen, or worse.

Money matters provide some of most compelling unanswered questions regarding the events of September 11, 2001. These questions point to possible darker truths, in part because of the incomplete and/or misleading treatments in official investigations to date. Pressing questions remain in at least three issue areas, including money transfers, suspicious activity reporting, and informed securities trading. In turn, cursory and misleading conclusions among relevant investigatory parties suggest a cover-up consistent with the possibility that the crimes of 9/11 were allowed to happen, or worse.

9/11-Money Transfers

In early October 2001, director of Pakistani intelligence services Lt. General Mahmood Ahmed was forced out of his position in the wake of published reports linking him to wire transfers totaling $100,000 into the bank account of alleged lead hijacker Mohamed Atta in Florida before 9/11. Ahmed was actually in Washington having breakfast with leaders of the U.S. Congressional intelligence committees on the morning of 9/11.

In early October 2001, director of Pakistani intelligence services Lt. General Mahmood Ahmed was forced out of his position in the wake of published reports linking him to wire transfers totaling $100,000 into the bank account of alleged lead hijacker Mohamed Atta in Florida before 9/11. Ahmed was actually in Washington having breakfast with leaders of the U.S. Congressional intelligence committees on the morning of 9/11.

Ahmed’s removal and the possible link to Atta’s financing were reported in U.S. as well as foreign media sources in late 2001. But the issue went unmentioned in the 9/11 Commission report. And on p. 172 of its final report the Commission apparently washed our hands of further investigative responsibility while concluding that “To date, the U.S. government has not been able to determine the origin of the money used for the 9/11 attacks. Ultimately the question is of little practical significance. Al Qaeda had many avenues of funding.” This shocking conclusion reeks of irresponsibility, at best, and its possible motivation is reflected in the Commission’s similar treatment of issues relating to possible informed/insider trading (see below).

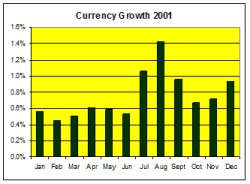

And there were far higher suspect amounts of money moving outside the electronic realm. Specifically, there was an extraordinary surge in currency shipments, billions of dollars of $100 bills, in July and August 2001. After a significantly above-average increase in July, the currency component of the M1 money aggregate (currency circulating outside of banks) rose in August 2001 at the then third-fastest monthly rate in the 650 months since World War II, trailing only December 1999 and January 1991. December 1999 was notable not only for pre-Y2K anxiety about bank accounts but also the millennium terrorist threat, while January 1991 was notable for the onset of U.S. military action in Iraq in Gulf War I as well as an important enforcement month in the B.C.C.I money laundering scandal. (The then-fifth-fastest growing month was, quite curiously, November 1980).

The August 2001 surge in currency shipments might be more innocently explained, at least in part, by a flowering banking crisis in Argentina, where demand for physical dollars arose among savers concerned for their bank accounts. But that crisis does not foreclose the possibility of two other very suspicious alternative reasons: precautionary pre-9/11 ‘wartime hoarding,’ and the possible use of currency in covert operations in Central Asia.

Under money laundering and other laws, banking assets can be frozen and seized in a time of war or national emergency. The United States had frozen Iranian assets in the 1979-1980 hostage crisis, for example, and used the same powers in responding to the African embassy bombings in 1998. In late 1999, too, the U.S. had blocked Taliban assets, and in October 1999, after the State Department designated al Qaeda as a terrorist organization, U.S. banks were directed to identify and seize those funds. The implied incentives may help explain the late 1999 surge in currency shipments, along with pre-Y2K anxiety.

Given that the U.S. had exercised these authorities in the past, and with warnings of a spectacular terrorism event on the radar screen in mid-2001, it is only natural to suspect that parties concerned that their assets might be at risk of being frozen and seized after the events of 9/11 were responsible for getting their assets out of the banks, into currency and, in turn, into safer underground assets like the diamond market. And this factor may have been at work in other countries with dollar-denominated bank accounts, like Argentina, as well as in the United States. Following that money trail could provide excellent clues about parties aware of, if not responsible for, the 9/11 attacks. But the currency shipments, totaling over $5 billion above an average for the July/August interval, and concentrated in $100 bills, are unmentioned in any of our official investigations to date.

In light of some of the work of Gould and Fitzgerald here at Boiling Frogs Post and their book Invisible History: Afghanistan’s Untold Story, a third explanation for the surge in currency shipments in mid-2001 arises. Negotiations over energy issues were underway with parties in Central Asia, including Afghanistan, in mid-2001, with U.S. representatives reportedly delivering military threats. These negotiations broke down in early August 2001, and covert operations aimed at Afghanistan could have already been underway in August 2001. (See this and this for some other background; at least one of these sources should be read, well, carefully.)

Currency shipments have a long history in U.S. covert operations, including for example the coup in Iran in 1953. They were certainly part of the U.S. operations in Afghanistan soon after 9/11. More recently, currency shipments have been part of the corruption of U.S. aid in Afghanistan, including how funds may have found their way into the pockets of our professed enemies. Any future honest and authoritative investigation of the events of 9/11 would explore the possibility that currency-funded covert operations were already in train in Central Asia soon before 9/11. This avenue of investigation would include exploration of related matters identified by Sibel Edmonds (see this, for example).

9/11-Suspicious Activity Reporting

On August 2, 2001, at a time when intelligence warnings of an impending terrorism threat were flowering, the Federal Reserve Board of Governors issued a non-routine supervisory letter to the Reserve Banks urging the importance of scrutinizing suspicious activity reports. This letter didn’t mention terrorism or its financing explicitly, but they were known and emphasized as important elements of anti-money laundering efforts. There was a significant increase in the number of suspicious activity reports being filed by financial institutions in July and August 2001, as well.

There is a related false statement in the final report of the 9/11 Commission. On page 186, while making a case that anti-terrorism efforts in the late 1990s and into the 2000s lacked focus on financial matters, the Commission stated:

There is a related false statement in the final report of the 9/11 Commission. On page 186, while making a case that anti-terrorism efforts in the late 1990s and into the 2000s lacked focus on financial matters, the Commission stated:

Before 9/11, Treasury did not consider terrorist financing important enough to mention in its national strategy for money laundering.

This statement was footnoted, with the footnote referring the reader to the 2001 National Money Laundering Strategy Report from the Department of the Treasury. In turn, in the underlying Commission staff monograph on terrorist financing, after making a case that ‘little attention was paid to terrorist financing,’ the monograph stated in footnote 26 that

The 2001 National Money Laundering Strategy, for example, issued by Treasury in September 2001, does not discuss terrorist financing in any of its 50 pages.

This statement is wrong, plain and simple. The words ‘terror’ or ‘terrorist’ appear 17 times in those 50 pages. The authors either didn’t do their homework, or were trying to tell a story. Terrorist financing was high on the agenda of anti-money-laundering efforts prior to 9/11. The NMLS reports for 1999 and 2000 also stressed terrorism and its financing, directly and prominently, as an important end to which anti-money laundering efforts (including suspicious activity reporting and analysis) were to be directed. And in the late 1990s the international Financial Action Task Force (the FATF, where the United States is significantly represented) repeatedly stressed terrorism threats in its international guidance. In turn, the U.S. Financial Crimes Enforcement Network’s “Suspicious Activity Report Review” dated June 2001 described a late-2000 FATF “Typologies Exercise,” where the major issues examined included terrorist financing as well as the role of cash vs. other payment methods in money laundering schemes.

Why did the commission and its staff state untruths? Could these statements have been part of a diversionary storytelling effort? Why might they have been trying to convince readers that anti-terrorism efforts and anti-money laundering efforts weren’t talking to one another, and weren’t ‘connecting the dots’?

One possibility is that the dots were indeed being connected, and information was indeed flowing between counterterrorism personnel and financial markets, including the banking regulators. There are two reasons the powers that be may have been particularly interested in downplaying this possibility, and emphasizing a misleading story regarding the lack of cooperation and communication. For one thing, the truth might reinforce how much information there really was out there regarding a threat, and open the door to the possibility the ‘attacks’ were effectively enabled, or worse. In turn, the information flow could relate to the third issue introduced above.

9/11-Informed “insider” trading

There aren’t a lot of $20 bills lying around on the sidewalks. If there were, people would have picked them up. For similar reasons, there aren’t a lot of ‘cheap stocks’ in the stock market. If there were, people would buy them, and bid up the prices until they weren’t cheap any more.

There aren’t a lot of $20 bills lying around on the sidewalks. If there were, people would have picked them up. For similar reasons, there aren’t a lot of ‘cheap stocks’ in the stock market. If there were, people would buy them, and bid up the prices until they weren’t cheap any more.

The securities markets are very efficient, in that they incorporate material information rapidly. The events of 9/11 certainly had material effects, on individual companies and the market in general. With the flowering of intelligence warnings in mid-2011, it is unreasonable to doubt that this information was being reflected in stock market trading activity.

A conference including the exchange community in Chicago was held soon after 9/11. A member of the audience posed a question for the panel, asking when we might expect parties to be prosecuted for the widely-believed insider trading that had been apparently taking place. An exchange community leader answered the question, stating that ‘this wasn’t insider trading,’ asserting the lack of any fiduciary obligation on the part of the traders to the companies at issue. That was when another member of the audience spoke up, loudly and out of turn, “well, maybe those people should just be prosecuted for murder.”

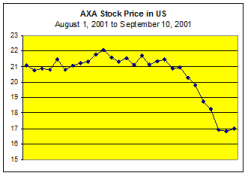

The airline stocks and related options on those stocks have been widely discussed, but another angle worth noting is the impact on the reinsurance companies. As people and companies buy insurance to protect themselves, insurers also buy insurance to protect themselves against large disasters. Munich Re is one of the oldest and largest reinsurers on the globe, and was exposed to huge losses on 9/11. From August 1 to September 4, 2001, Munich Re’s stock price fell 8%, and then fell sharply further the week before 9/11, another 13% in a single week. Munich Re had company among the insurance company. A large French insurance firm with 9/11 exposure, AXA, has some publicly traded equity here in the United States. Here’s how its stock price looked the weeks before 9/11:

AXA’s common stock fell almost 20% in the week before 9/11.

As people buy insurance, and as insurance companies themselves buy reinsurance, so can investors hedge their exposure (or amplify it) via the derivatives markets. One instrument that has gained a lot of attention in recent years is the CBOE “VIX” index. This index is based on options prices, and has gained the nickname ‘the market fear index’ because it can capture market uncertainty, an important element for anyone watching the financial market crisis in recent years.

So, how did the ‘market fear index’ do in the weeks before 9/11?

From August 24 to September 10, 2001, the VIX index rose over 60%. Such an increase over a 10 day trading period has happened less than one-half of 1 percent of the time since the introduction of this index in 1990. It climbed sharply higher after 9/11, to be sure, but the increase before the event is consistent with information about the event flowing into the financial markets.

This isn’t proof, of course, but the existence of trading on some form of 9/11 information before the event is not to be unexpected, in light of the extent of intelligence warnings. But that is what makes the 9/11 Commission’s treatment of this issue disturbing. The Commission chose to take adopt ‘al Qaeda didn’t do it, therefore, there wasn’t any informed trading before the event’ posture. For example, on page 171-172 of the final report, the Commission stated:

There also have been claims that al Qaeda financed itself through manipulation of the stock market based on its advance knowledge of the 9/11 attacks. Exhaustive investigations by the Securities and Exchange Commission, FBI, and other agencies have uncovered no evidence that anyone with advance knowledge of the attacks profited through securities transactions.

And in a footnote to this finding, the Commission cited how an investor with ‘no conceivable ties to al Qaeda’ was responsible for significant volume in one transaction of interest. There is no affirmative evidence the Commission investigated the possibility that information arriving through intelligence and/or financial regulatory agencies was also finding its way into the markets, even though al Qaeda wasn’t itself doing the trading. The Commission’s conclusion cited above may not be an entirely accurate depiction of what the SEC and other parties did or didn’t find, but in any event, the 9/11 Commission wasn’t charged with finding out what other parties in the government found out. The Commission was charged with making its own determination.

Where Do We Go From Here?

The issues of pre-9/11 money transfers, suspicious activity reporting, and informed securities trading couple with the incomplete if not purposefully misleading official investigations to leave us with still-open questions that won’t go away. These three issue areas are not the only financial matters that remain worth investigating, and they couple with other scandalous elements suggesting negligence, or worse.

The thousands of deaths on 9/11 were multiplied by many thousands more for innocent civilians and, speaking of money, billions of our dollars spent (and received, by those who were enriched) in our military responses to a set of still-unsolved crimes. Yet there seems to be few signs that our Ship of State (including its mainstream media handmaiden) will ever revisit its course. It can make you wonder if it’s time to hang up the cleats and get on with life.

But this is America, and we still have patriots.

Press For Truth, the movie title goes. We will get there, wherever it is.

Bill Bergman- Senior Financial Analyst, ‘Follow the Money with Bergman’ at Boiling Frogs Post

Bill Bergman- Senior Financial Analyst, ‘Follow the Money with Bergman’ at Boiling Frogs Post

Bill Bergman has 10 years of experience as a stock market analyst sandwiched around 13 years as an economist and financial markets policy analyst at the Federal Reserve Bank of Chicago. He earned an M.B.A. as well as an M.A. in Public Policy from the University of Chicago in 1990. His favorite course there was titled “The Economics of Regulation,” and the lessons learned in that course and elsewhere help illuminate his cautious if not cynical and concerned perspective when told that government is looking out for us. Mr. Bergman is currently working with Social Movement Sciences LLC, a new enterprise developing evaluation and funding services for not-for-profit organizations. He is married, with three kids, and lives in Chicago. His objective with this column is to provide insight into financial and economic conditions, public policy framing money and financial markets, the history underlying our financial infrastructure, and monetary aspects of investigations and scandals.